1.0 IDBs IN REVIEW: PLAYING AN IMPORTANT ROLE BUT JUST NOT WINNING AN OSCAR

The interdealer brokers IDBs) are transactional in business and mindset. Their current role maintaining interest in less liquid markets through price discovery is not only understated, it fulfils a vital role, especially as Banks become less and less willing to publish indicators themselves thanks to regulatory pressure. This places a greater emphasis on their ability to connect counter-parties by both electronic and non-electronic channels without which trading in some instruments could simply dry up.

The problem the IDBs have is also their advantage. Fully electronic markets because they are highly efficient for liquid markets, become more inefficient as liquidity decreases (players do not want to expose themselves) but once a market hits critical mass and a market goes electronic, the IDBs higher cost structure (i.e. people) forces them out (FX, USTs). On the other side financial markets are inherently innovative which offers IDBs new opportunities.

- The combined 2022 total revenue of the Big 4 Brokers was US$6,798 Million. This represents 6% growth over 2021

- The combined 2022 total data & analytics revenue of the Big 4 Brokers was US$345 Million. This represents 8% growth over 2021

NEED TO BUILD UP DATA & ANALYTICS BUSINESSES

Tradition’s 2022 Annual Report succinctly assessed the opportunities and predicaments faced by all the IDB’s information services businesses.

‘Clients are looking for independent sources of reliable price and volume information for OTC markets, and the addressable market is expanding for realtime, end of day, historical data sets and also analytics. Tradition and its peers are also lagging behind the exchanges in terms of ability to monetise their data assets.’

In the OTC markets even more than exchanges, data and analytics drives trading back to the venues. IDBs produce trade to create activity which results in execution. The IDBs must unlock unmonetised data both to improve their trading volumes, meaning more commissions, and build higher revenue generating information businesses.

In an ever more data centric world the IDBs must invest more in information services, data and analytics.

2.0 2022 IDBs IN REVIEW: KEY EVENTS

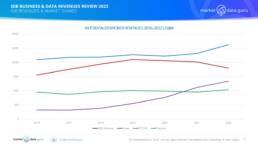

- These leading 4 IDBs had estimated revenues for all business activities of $4928 Million in 2016 which grew to $6,798 Million in 2022, i.e. an increase of 38% over the period.

- In contrast the IDBs data and analytics had combined revenues of $195 Million in 2016 which increased 77% by 2022 to reach $345 Million.

- BGC Group and TP ICAP venture further into crypto territory

- Marex maintains its third place by annual revenue generating US$1,344 Million with growth coming from acquisition

2.1 2022 IDBs IN REVIEW: OTHER EVENTS

- Apr 2022 BGC’s Sunrise executes first block trade of Micro Bitcoin options from CME Group

- May 2022 FCA approves TP ICAP’s application to become an authorised benchmark administrator

- Aug 2022 Marex agrees to purchase of ED&F Man Capital Markets for US$220 Million. Marex could well be set to challenge BGC Partners and TP ICAP as it expands beyond commodities into fixed income. This does not appear to be the last of Marex’s acquisitions, at least until it has bulked up enough to finally IPO

- Aug 2022 TP ICAP’s Parameta with partner PeerNova launches new enhanced consensus pricing solution ‘ClearConsensus’ for risk and capital management

- SEP 2022 According to Sky News shareholders want to spin TP ICAP’s data & analytics business, Parameta, out of the group estimating its value at GB£1.5 Billion. Only problem is this they haven’t worked out that the data generation is intrinsically linked to TP ICAP’s front desks., or if they have looking to score a cheap and very short term win

- Nov 2022 BGC Partners rebrands as BGC Group

- Dec 2022 TP ICAP obtains crypto exchange licence

- Dec 2022 Tradition completes buy of MTS Markets International from Euronext’s MTS and obtains MTS BondsPro an electronic credit trading platform that offers access to liquidity and real-time execution on its anonymous, all-to-all order book

4.0 2021 BUSINESS REVENUE HIGHLIGHTS

- From 2016 onwards Marex easily produced the largest overall revenue growth of 307% driven by an aggressive acquisition strategy. While 2022 was not as active as 2021, the purchase of ED&F Man Capital Markets provides critical mass beyond commodities and energy

- However, Marex’s data & analytics business remains an afterthought

- TP ICAP saw a positive increase in revenues over 2021 by 13%, something investors still do not recognise

- In contrast BGC Group’s revenues plateaued in 2019 and last year saw a decrease of 11%

- Tradition’s income grew 8% year on year to 2022

- BGC Partners and TP ICAP combined market share declined from 68% for all businesses in 2021 to 64% in 2022, reflecting a long term growth and the rise of Marex

- In contrast, the top 2 brokers data & analytics business (Fenics & Parameta) maintain a substantial market share of 92% in 2022 compared to 2021’s 93%. The minor decrease coming from increased competition from Tradition

- In 2022 the IDBs percentage of revenues from data & analytics, which was the same as the previous year, 5%, continues to lag significantly behind exchanges

4.1 2022 MARKET DATA REVENUE HIGHLIGHTS

- Each of the IDBs data businesses have unique OTC market coverage, albeit with content overlap, leading to different prices for many of the same instruments depending upon source.

- This works to the IDBs advantage because financial institutions demand a minimum of 2 sources for OTC markets

- Although TP ICAP and BGC represent 92% of the IDB’s data revenues, they do not produce anywhere near the same percentage of prices and data generated, i.e. there is more data that can be commercialised

- Tradition continues to onboard new sales people in a renewed bid to increase revenues, with particular focus on the Asia-Pacific region

- The challenges faced by IDB’s data businesses in 2023, and how these should be met, remain similar to those of 2022.

- While Cloud connectivity offers additional prospects especially given their unique range of OTC content accompanied by its natural synergies to value added premium services, i.e. analytics, the IDB’s in-built aversion to technology and spending money could well be hindering potential opportunities

8.0 PEER REVIEW MARKET DATA & INFORMATION SERVICE REVENUES

Unlike their exchange equivalents (excluding the US and to an extent UK/European Equity markets), the IDBs do not have a relatively captive domestic market which underpins their information services business.

What they do have is a far more diversified audience with a global presence, while competing head to head with each other by leveraging their relative strengths and weaknesses across asset classes. Importantly although each IDB offers prices across multiple markets, in the same market (i.e. Bonds) the volumes and values will be different. There is no OTC equivalent to the Consolidated Tape, and unlikely for some time for non electronic traded markets.

KEY POINTS

- Exchanges with larger data & analytics revenues than the IDBs are more diversified businesses vertically, often with significant index services, and vendors in their own right

- In income terms TP ICAP and BGC are broadly comparable to Tier 2 Exchanges whose information businesses are still primarily driven by underlying trading prices and yet to expand

- Tradition is renewing its focus on market data has recognised the value of people skills, but still needs to integrate more front office data from across its global dealing desks to broaden breadth and appeal.

- Marex brokers critical commodities, energy and freight markets and now potentially Fixed Income, producing unique high value data it is still disinterested in monetising

11.0 2023 REPORT CONCLUSIONS: LOOKING FORWARD

The conclusions that MDG reached regarding IDB’s revenue growth in 2022 remain just as relevant in 2023, actually more so.

- Voice and hybrid broking has its place in the market. There are things humans can do which automated processes can’t, especially where complex multi-leg transactions involve less liquid markets, and there is difficult price level discovery.

- Such deals also entertain a premium, but the IDBs must accept that this is at best a declining market in percentage share terms.

- Inevitably, the ability to trade electronically will always trump voice, if only because of costs and client demand.

- The option the IDBs have is to sunset their own services before others do it for them, by moving existing voice brokerage services over to electronic trading at the earliest opportunity, which means planning in advance, not exactly the IDB’s strong suite. Certainly this will not be a popular choice but there might not be a viable alternative if the IDBs want to remain relevant

Data as always is at the heart, especially if Bloomberg and Refinitiv are the IDBs two single largest dollar clients. There is plenty of opportunity for IDB’s to develop value added information related services compared to other data sources like the exchanges, if only because of their broad coverage across asset classes and unrivalled global presence. The IDBs should be leveraging their IP rights more effectively by building around consumer usage to create new revenue streams relatively rapidly. The opportunities are there.

11.1 SUMMARY

MDG places a great emphasis on data & analytics to any trading venue’s future, it is existential, but the ability to offer information services depends upon the business as a whole, which at its core is that trading. The persistent emphasis on transactional based tactical decision making over strategic clarity will continue to hamstring the IDB’s undoubted future potential. Until this legacy thinking changes there will be no Oscars.

Next week we shall analyse the IDB’s market capitalisation

Keiren Harris

06 June 2023

For our information on our consulting services get in touch and please visit www.marketdata.guru/data-compliance

Or Email knharris@marketdata.guru

General contact info@marketdata.guru and to obtain a pdf copy of the article