PEER REVIEW

The days of venues being one trick ponies (well the big ones anyway) focused on single markets with little local competition have long gone. They are now complex businesses which compete globally, offer services right the way across the trading and data workflow cycle, and have expanded into offering related information services and trading systems to help drive trading back into their multiple venues.

Given the important roles venues play in capital markets comparing their diverse businesses by revenue, and how investors value these businesses provides a range of intriguing insights.

HIGHLIGHTS

- The total revenues of all 20 venues year ending 31/12/2022 was US$61,083 Million, up 7% on the previous year

- Exchanges saw the largest increase at 9% followed by the IDBs at 6% while the electronic brokers declined -7%

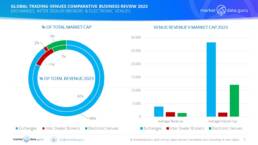

- The combined market cap of the 20 venues on 31/03/2023 totalled US$409,024 Million

- The top 6 venues are all exchanges with a global presence and are the most diversified, especially in offering data, analytics and multi-asset class trading, accounting for 67% of total revenues in 2023

- Of the other 7 exchanges, only 1 has a significant data & analytics business (SIX), 1 has multiple (3+) venues (Euronext) but lacks a progressive market data business, while the other 5 primarily focus on their domestic markets, yet to develop their information services

- Despite the people intensive IDBs being 7th, 10th, 13th, and 15th, by revenue, they rank in the bottom four by market capitalisation

- The electronic venues which are tech intensive, not people reliant, are ranked 8th, 14th , and 20th, by revenue though 7th, 8th and 16th by market cap. It is interesting to note 8th ranked Virtu which is a major dark pool operator is lowest by market cap in this category

The table below ranks the 20 venues by revenue and market capitalisation. Note: Marex and SIX’s market cap are calculations based on a comparative Price/Sales ratio

INFORMATION LEAD STRATEGIES

Investors prefer tech intensive over people based businesses, and those which have developed strategies to expand into offering fully electronic trading in OTC markets, along with traditional exchange based venues, and leverage information services and data processing to offer a complete end to end experience.

The leading exchanges have deliberately avoided developing new data and analytics businesses in-house. Buying in established companies with products already embedded in their clients is a far more effective approach because it simultaneously brings in new customers which also want related information services and ready made revenue streams.

A direct result has been the interest Big Tech, notably AWS, Google, and Microsoft has taken in building deep partnerships with leading exchanges, CME, DBAG, LSEG, and NASDAQ. There is always an outlier, ICE has avoided such tie ups seeing itself as a technology based trading environment in its own right.

It is noticeable exchanges and electronic trading venues do not enter OTC markets until liquidity has reached the level where automation of trades has pushed traditional brokers out through undercutting their margins to a point they cannot compete. However the IDBs have the advantage they can create complex deals which straight tech cannot. Both automation and complex trades require data, and this should place an emphasis on data led approaches to revenue generation.

RESULT

- The Price/Sales ratio of Exchanges is 7.32, slightly lower than the electronic venues at 8.52 but both significantly higher than the IDB’s 0.93

- Average revenues of the Exchanges is US$3,847 Million, but there is a divergence between the top 6 exchanges which average US$6,809 Million (of which a major percentage is information and trading services) with the other 7 averaging US$1,308 Million

- In comparison the IDB’s average revenue is US$1,699 Million and electronic venues is US$1,424 Million, both above the lower 7 exchanges

VENUES AND THE FUTURE

Venues that realise the execution of a trade is only one part of the complete trading workflow are rapidly differentiating themselves from their peers in terms of the breadth of services on offer and the revenues they can generate. Something the market is noticing, and with greater market capitalisation comes financial firepower to further enhance presence and opportunity, especially when backed by Big Tech.

This enables them to expand into other markets globally. The focus on trading cycle products and information services, in particular unique datasets like indices, is somewhat driven by necessity. In the US, UK and EU regulators will almost certainly prevent further concentration in exchanges, and outside those markets political imperatives prevent acquisitions.

Nobody seems to want the IDBs until they develop, and crucially articulate, new strategies. Though the regulators probably would not be averse to a combination of IDBs merging, except possibly TP ICAP/BGC Group which would probably be the marriage from hell in any case.

In any event information services, data and analytics, and where and who by the data is processed are the keys to every venue’s future success.

Talk to us about our consulting, and our independent advisory services

Keiren Harris 27 June 2023

For information on our consulting services please email Knharris@marketdata.guru

https://marketdata.guru/data-compliance

Please contact info@marketdata.guru for a pdf copy of the article

#brokers #IDBs #marketdata #exchanges #analytics #LSEG #NYSE #NASDAQ