BREAKING OUT FROM OLD MINDSETS

Price Discovery.

These two words define what the Inter-dealer Broker (IDB) business is all about. Finding the right market level so that third parties can trade with other. This means data, yet the IDBs have until relatively recently been both technophobic, preferring traditional voice broking, and dataphobic, not truly comprehending what data means to their underlying business.

It is this lack of understanding which could become problematic for the future, as certain brokers first begin to realise the true value of their data businesses and then seek to exploit it. The fact that BGC Partners differentiates its data business by using the old GFI ‘FENICS’ name, and TP ICAP has recently rebranded its data & analytics services to ‘Parameta Solutions’ (To think someone got paid to come up with that) could be indicative of intentions. We will return to this later.

This Report

This report analyses the IDBs from a high level with specific emphasis on the importance to all IDBs of the datasphere. Included are the 3 ‘majors’, BGC Partners (BGC), TP ICAP (TPI), and Tradition (TFS), plus Marex Spectron (MS) which re-branded in April 2021 as just ‘Marex’.

Marex is unlike its peers by not being listed and ever since Foshan’s failed takeover attempt the broker has adopted a strategy of aggressive expansion via acquisition.

Four brokers sounds like an oligopoly, however, the Interbank market is rife with cutthroat competition from companies of all shapes, sizes and flavours.

2020 and 2021 Years of Change

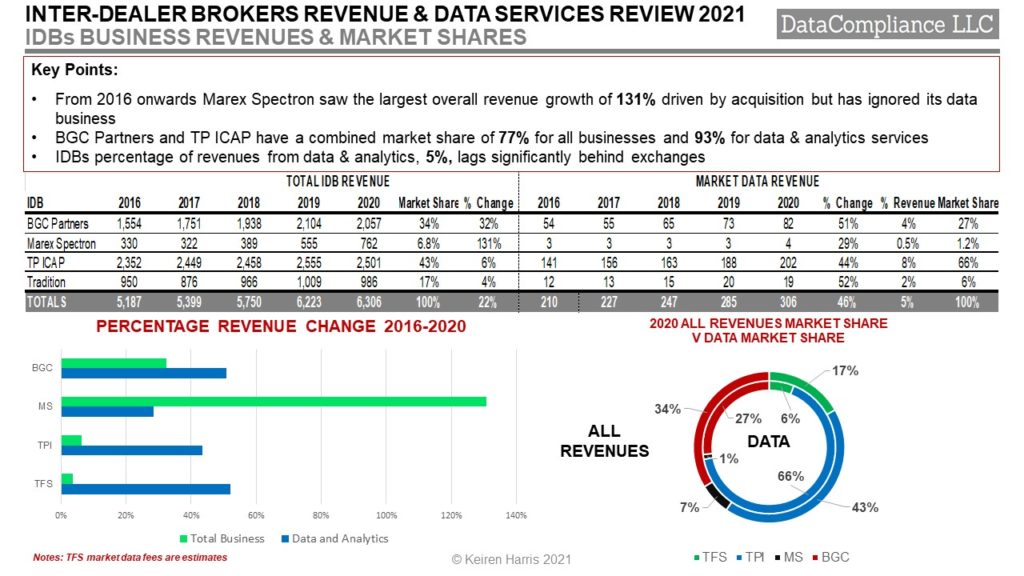

• These leading 4 IDBs had estimated revenues for all business activities of $5,187 Million in 2016 which grew to $6,223 Million in 2020, i.e. an increase of 22% over the period.

• In contrast the IDBs data and analytics had combined revenues of $210 Million in 2016 which increased 46% by 2020 to reach $306 Million.

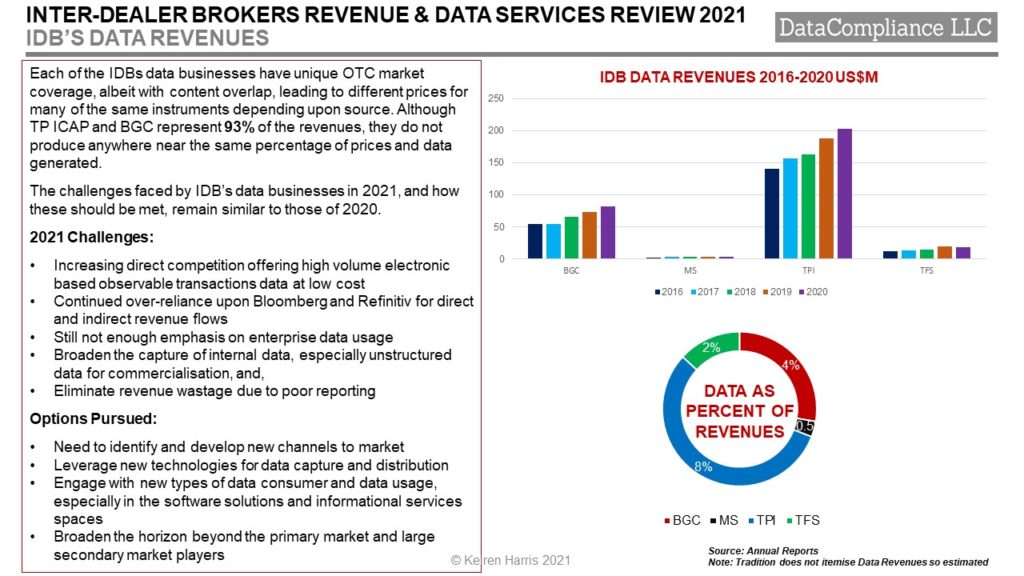

On its own this increase in the IDBs reliance upon market data, information services, and analytics reflects a recent trend away from core traditional voice broking services to offering broader value added services, which are more commercially data friendly. As these opportunities are not going to be found internally, this means going out-of-house for already established business in 2 areas as well as a continuation of IDBs swallowing up smaller, specialist, competitors.

- Embracing Electronic Markets. The IDBs have never been electronic broking friendly, however while TP ICAP’s Liquidnet purchase ($750 Million) may have been opportunistic, it is a definite strategic move into markets that are growing faster due to the way they are traded, while generating high quality price data. BGC focused on FENICS GO (Global Options) to obtain a wider electronic trading footprint, and Tradition teamed up with MTS to create the MTS Tradition European Asset Swaps data service

- Post trade solutions. Again, TP ICAP has taken a lead by expanding its post trade risk management services through launching ‘Matchbook Re-Balance’ for bond markets, which neatly fits in with Liquidnet, while MS got its new Marex Clearing Services up and running

- Continued IDB Consolidation. The IDBs still see their smaller siblings as a threat, and elimination through acquisition is one strategy with Louis Capital bought by TP ICAP ($21 Million) and MS stayed in spending mode buying StarSupply and X-Change Financial Access

Each of these moves are data friendly, the IDBs increases their underlying content which can be exploited through providing analytic services

OPPORTUNITIES & CHALLENGES

Market Perspectives

Why does the market not appreciate the IDBs? It appears among investors and research analysts there is a lack of understanding about what the IDBs really do. Their presence and function leads to price discovery, creating liquidity for markets which otherwise would be less efficient and stagnate. By implication the IDBs are poor at self-promotion.

Branding and Spin-Offs?

Brands are an incredibly valuable commodity and often sell a product rather than the other way round. So keeping an entity distinctly separate as BGC has done with FENICS, or re-branding the corporately titled TP ICAP Data to ‘Parameta Solutions’ raises a single question, Why?

The logical conclusion would be to spin off the business to unlock the undoubted value. As we have demonstrated the IDBs data & analytics subsidiaries (excluding Marex) comfortably outperform the underlying business, so there is obviously a reasonable case. But is it a good case? These data businesses are almost 100% reliant upon the goodwill of the brokerage businesses, a spin-off inevitably changes that dynamic. This is definitely a spot to watch in the coming months.

Conclusion

I have long argued that the IDBs need to evolve and leverage their data more effectively. It seems over the last 12 to 18 months that is happening. Whether this has come about by strategic design or lucky opportunism, which itself shows ability to spot then take advantage of a situation, this is altering overall businesses balances, by leveraging the core services, then adding value (that can be premium priced unlike much of the broking) which did not previously exist.

Data as always lays at the heart of the IDB world with plenty of opportunity for the brokers to develop basic information related services in wider range of markets when compared to other data sources like the exchanges.

Keiren Harris 06/05/2021

Please email knharris@marketdata.guru for a pdf or information about out consulting services