2023 MARKET PERSPECTIVES

Why does the market not appreciate the IDBs? It appears among investors and research analysts there is a lack of understanding about what the IDBs really do. Their presence and function leads to price discovery, creating liquidity for markets which otherwise would be less efficient and stagnate. By implication the IDBs are poor at self-promotion.

Equally the market tends to be a bit geeky, there is a preference for technology and more politically correct stocks, and the IDBs are rarely if ever accused of being either. Yet certain market trends like ESG investing, more volatility in OTC asset classes which have only just started the transition to electronic trading like Energy, soft commodities and metals ought to focus the IDB’s management attention on the potential to get in on the ground floor this evolution instead of spectating while others steal their lunch.

HIGHLIGHTS OR LOWLIGHTS?

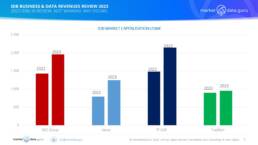

The combined market cap of the IDBs grew 37.1% from 18/04/2022 to 31/03/2023, i.e. $4,600 Million to $6,306 Million, however these performances are all from a very low base, but at least heading in the right direction. For perspective the smallest of the Tier 1 exchanges, TMX had a market capitalisation of $6,022 Million and SGX the second smallest $7,398 Million

Investors do not value the IDBs anywhere close to the exchanges.

- BGC Group grew 37.1%

- Marex is unlisted, therefore its notional market cap based on a calculation of Price/Sales ratio increased the most at 57.6%

- TP ICAP despite pressure from shareholders rose by 44.8%

- Tradition increased by a more modest 6.2%, however like for TP ICAP impacted by exchange rates

The combined price/sales ratios of the IDBs was 1.05, in other words the value of the businesses is almost identical to the annual revenues, and even then Marex is the only one of the IDBs that is above 1. Again, we can see this is very low compared to TMX’s 7.3 and SGX’s 8.9

BRANDING & DATA BUSINESS SPIN-OFFS

Brands are an incredibly valuable commodity and often sells a product rather than the other way round. Keeping an entity distinctly separate as BGC has done with FENICS, or re-branding the corporately titled TP ICAP Data to ‘Parameta Solutions’ raises a single question, Why?

The logical conclusion would be to spin off the business to unlock undoubted value. As MDG has demonstrated the IDBs data & analytics subsidiaries comfortably outperform the underlying business, so there is obviously a case. But is it a good case? These data businesses are almost 100% reliant upon the goodwill of the brokerage businesses, a spin-off inevitably changes that dynamic. Parameta has been over-optimistically valued at £1.65 Billion, as much as parent TP ICAP, making it an obvious target for unhappy shareholders.

This is definitely a spot that will keep being returned to, especially if shareholder pressure continues owing to poor share performance, and managements seek what might appear at first to be an easy option. However, it is a game without winners, except those shareholders looking to take the money and run as soon as possible. What happened to Air Canada’s Aeroplan ought to send out strong warning signals.

SUMMARY

As stated in a previous analysis of CME by MDG, one way to judge one’s value is to have others measure it for you. In financial markets that measure is the market capitalisation.

If so then the market continues to undervalue the IDBs at their true potential, which is certainly not close to exchanges or listed Multi-lateral Trading Facilities (MTF/ATS).

Where Problems Lie:

- Low Credit Ratings due to low balance sheet utilisation.

- Lack of research coverage

- Need to grow and develop their data and analytics businesses

- Poor PR, the IDBs do not explain themselves well to the market

The key to the IDBs is they are intrinsically a people, not capital, intensive business. It is unfortunate the modern investor sees people not as a strength but merely a cost to be eliminated in favour of technology

Keiren Harris

13 June 2023

For our information on our consulting services please visit www.marketdata.guru/data-compliance

Or Email knharris@marketdata.guru

General contact info@marketdata.guru and to obtain a pdf copy of the article