2021 EXCHANGES AFTER 10 YEARS OF CHANGE

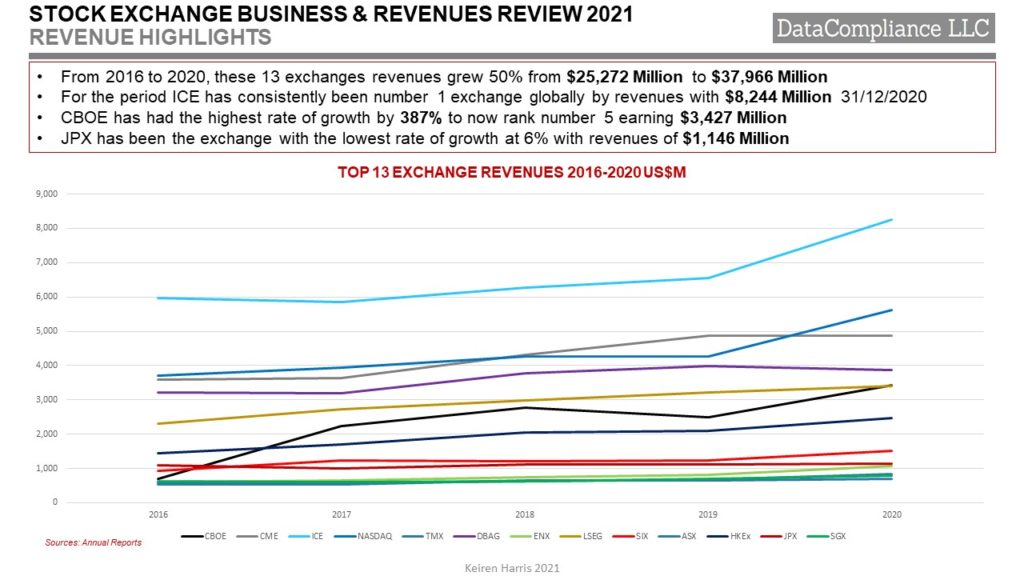

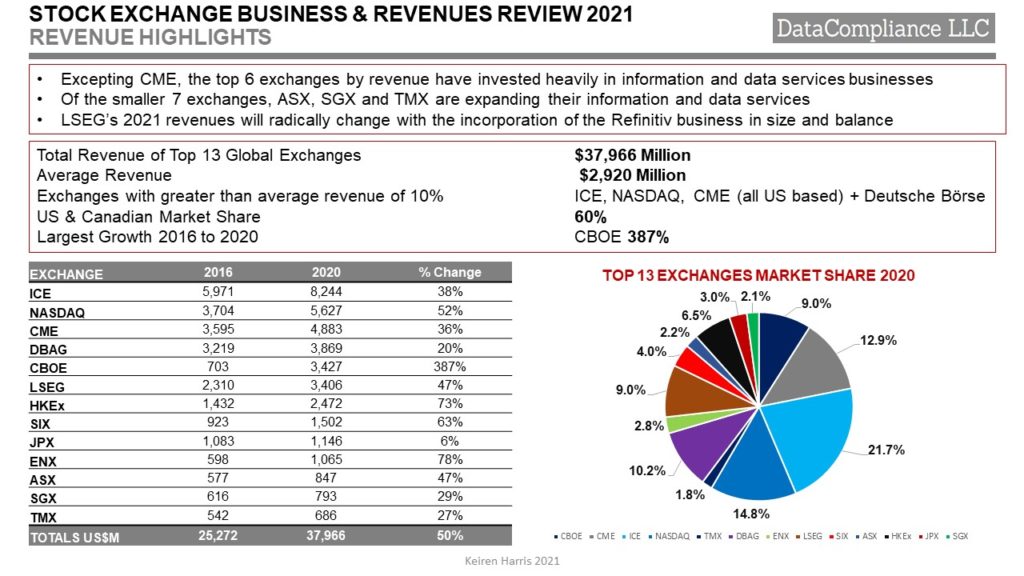

The leading 13 exchanges estimated revenues for all business activities grew from in 2016 $25,272 Million to 2020 $37,966 Million, i.e. an increase of 50% over the period.

The 13 exchanges are Australian Securities Exchange (ASX), CBOE Global (CBOE), Chicago Mercantile Exchange (CME), Deutsche Börse (DBAG), Euronext (ENX), Hong Kong Exchange & Clearing (HKEx), Intercontinental Exchange (ICE), Japan Exchange (JPX), London Stock Exchange Group (LSEG), NASDAQ, Singapore Exchange (SGX), SIX Swiss (SIX) and TMX Group (TMX).

2020 proved to be a far more interesting year than most people expected, and definitely not wanted. The Covid-19 bear market began on 20/02/2020, ending 07/04/2020, with most markets not fully recovering until the end of the year, and while the headline story definitely was not the only driver of financial despair.

Yet 2020 must not stand in isolation, the big Stock Exchanges are now vastly different beasts to their counterparts of 2010, and there have been very clear trends over the decade, with differences in terms of strategies for the more innovative groups seeking to reduce reliance upon traditional commissions and IPOs.

- Consolidation. The largest exchanges have been active in acquiring competitors, CME consolidating commodities futures venues, NASDAQ and smaller exchanges, ICE taking over NYSE and LIFFE while spinning off Euronext which has gone on a purchasing rampage across Europe taking in Irish Stock Exchange, Borsa Italiana/MTS, Oslo Børs, and Nord Pool

- Market Diversification. Becoming more heavily involved in clearing, and entering liquid, electronically traded OTC markets, focusing on FX (CBOE/Hotspot, Deutsche Börse/360T, Euronext/Fastmatch) Fixed Income (CME/NEX, NASDAQ/eSpeed) and Commodities (TMX/Trayport)

- Buying into Data. Although the banner headlines have been ICE’s purchase of Interactive Data, and the LSE/Refinitiv merger, exchanges have been highly active in buying index businesses (DBAG/STOXX, LSE/FTSE Russell), analytics providers, and other investment decision tools (CBOE, DBAG, ICE, LSE, NASDAQ)

Key Events for 2021

• Euronext’s ‘continental’ strategy continues with the purchase of Borsa Italiana, the Irish Stock Exchange, and Oslo Børs

• Completion of the LSEG/Refinitiv merger which has already seen LSEG forced into spending $1,370 Million (£1 Billion) on integration costs, the announcement of which promptly spooked the markets. Refinitiv revenues are not included in this report as the merger did not complete until 2021, though the impact of the market cap is.

• This is the first example of a combined exchange venue/market data business where the data side is larger than the venue

These 2 events demonstrate and emphasise the difference between exchanges adopting a horizontal integration strategy and a vertical integration strategy

Key Trends in 2020

• Diversification may bulk up revenues but does not necessarily equate to the highest revenue growth, and the exchanges can be roughly divided into two groups, a more diversified club of 6, and a less diversified collection of 7

• Arguably the most diversified club of CBOE, DBAG, ICE, LSE, NASDAQ, and SIX had a combined revenue growth rate of 55% over the period 2016 to 2020, with CBOE achieving a growth rate of 387% and SIX 63%, but in both cases the growth was driven by core venue businesses, and in SIX’s case certainly not from its long time data business SIX Financial

• The diversified club of exchanges had combined revenues of $26,075 Million in 2020

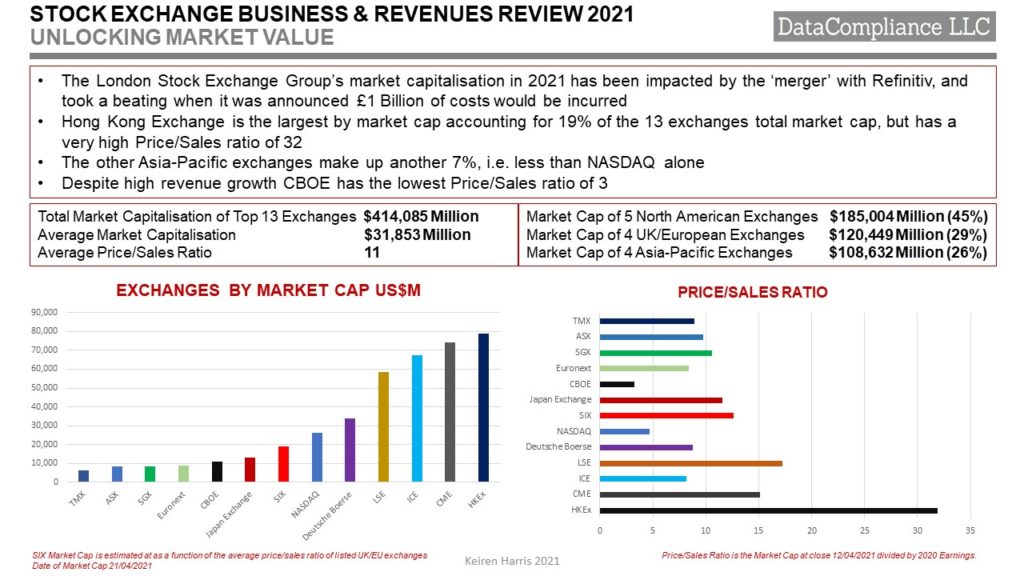

• As of 21/04/2021 these exchanges had a total market cap of $216,366 Million

• In comparison the less diversified exchanges, ASX, CME, ENX, HKEx (the least diversified exchange of the group), JPX, SGX, and TMX achieved a combined growth of 41%

• The less diversified group of exchanges had combined revenues of $11,891 Million in 2020

• As of 21/04/2021 these exchanges had a total market cap of $197,718 Million

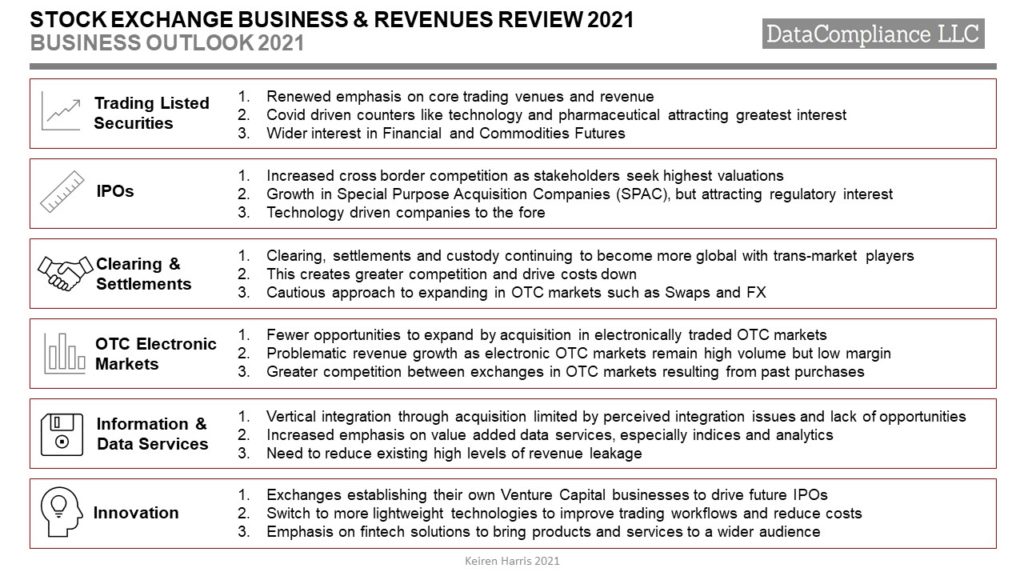

FUTURE CHALLENGES

2021 Impacts

Covid 19 was unforeseen and is having wide ranging impacts which for exchanges seems to have leave them struggling for strategies for a post-virus future

• Many exchanges appear to be stuck in ‘administration’ mode avoiding making decisions about where the business is going next, especially in their information and data services units

• Regulators are putting more pressure on exchange’s data businesses, especially ESMA, without understanding it

• Exchanges with a high technology listings contingent have done exceptionally well according to McKinsey’s recent report on the impact of Covid-19 on capital markets which has played well to exchanges like NASDAQ, and HKEx, with their ‘Mega 25’ adding US$5.8 Trillion in value in one year, i.e. 40% of total global gains

• The development of Special Purpose Acquisition Companies (SPAC) is now attracting technology companies that once would have listed on their local exchanges to already tech heavy markets like NASDAQ, reinforcing a dominant position

2021 Summary

• The largest exchanges have transitioned from domestic venues to diversified entities trading globally

• Growth has been through acquisition rather than organic, which is unsurprising, given the largest exchanges were reaching saturation point in their own local markets

• Opportunities for horizontal integration is becoming increasingly thinner as the pool of available exchanges yet to be pulled into a larger grouping shrinks

• While exchanges have extensive financial firepower based upon market cap, they are quite cash poor, which further constrains potential expansion

All the exchanges face challenges, but there is a constant, the tendency to diversify is greater for the exchanges facing the most competition in their core trading venues business.

Keiren Harris 30/04/2021

Please email knharris@marketdata.guru for a pdf or information about out consulting services