MYTHS & REALITIES

Back in 2010 I was advising a large Japanese Investment Bank and I stood directly behind the Fixed Income desk analysing how they used price data. Edward, a bond salesman whose every third utterance included “My Bloomberg” was busily engaged on a speaker conference call with his traders and a rather influential asset manager. The unfolding short chat illustrates the sub-liminal role Bloomberg plays within the market.

Edward “My price on the UST30 Year is $99.4531”

Client “Sounds expensive”

Edward with a certain arrogant finality “Well that’s what My Bloomberg says”

Client “Ah, okay, that explains it, I don’t use Bloomberg” (Well there is always one)

Edward “How can you be an asset manager without a Bloomberg?” In talking to Edward I found he was unaware other vendors even existed, nor for that matter Interdealer Brokers. His Bloomberg terminal was both the Bible and St Paul rolled into one oracle.

Client “You @#%*!” So ended the call, and the relationship.

The point? Bloomberg has become, or at the very least, perceived to be the indispensable company in capital markets, today.

Bloomberg is now so deeply entrenched in financial markets were it to magically vanish tomorrow, meltdowns would quickly follow. Without market data there are no financial markets because it provides the raw material to base investment decisions upon, and this is where Bloomberg offered something radically different when it launched.

Hyperbole? No. Until the 1990s (long after Bloomberg started) Reuters and Telerate ruled the roost over the Foreign Exchange and Equity markets with their price data and news driven terminals, Telerate’s Page 500 was home to Cantor’s proprietary US 30 Year Treasury price, the benchmark written into many contracts. Bloomberg had first entered the underserved Fixed Income markets with its analytics based product, it provided prices with decision tools, the key differentiator, with a ready made clients on shareholder Merrill Lynch’s Bond desks. The launch of its infamous Bloomberg messaging system helped build a closed, even fanatical, and expanding community. Asset managers would tell their brokers they would only communicate with their brokers via Bloomberg IM forcing the sell-side to migrate wholesale. Aided by arrogant competitors wallowing in their own incompetence enabled Bloomberg to prosper.

THE FIRST CLOUD

Built on 1950s era Fortran code it may seem strange to describe Bloomberg as the first cloud. Yet if we think about it Bloomberg has been doing for years what the recent BigTech/Big Exchange partnerships are just beginning to put in place now. Unlike the PC based competition Bloomberg does virtually everything on its own mainframes, in its own proprietary environment. A Bloomberg user can access price data, carry out analysis, calculate risk and margin, value portfolios, and trade all in one place using Bloomberg’s own tools or those from third parties because it can all be done on Bloomberg’s own infrastructure. Smaller financial institutions could now carry out virtually all their trading workflows in one place. By the time Reuters responded and was the only vendor that did, Bloomberg had moved on even further ahead.

GROWTH

Despite raising its high fees every time a contract rolls over, Bloomberg has defied the most determined CFOs and tenacious market data managers to expand its presence to the point where it overtook Thomson Reuters as the number one vendor by revenue in 2011 and now commands a market share of 31% amongst the top 9 vendors with market leading revenues of $12,200 Million, up 336% on 2002.

Unlike its two main competitors Bloomberg’s growth has been organic, built around terminals. Its limited M&A has proven mixed, the Barclays Indices more successful than Polar Lake.

In contrast Reuters has lived Trotsky’s nightmare of permanent revolution, merging with Thomson’s, and constant re-organisations Reuters and its successors managed to destroy value in acquisitions, lost market share and is now emerging from two lost decades with more focus as a LSEG subsidiary.

S&P has progressively expanded through smarter acquisitions of analytics based services and index providers to become an IP based index/credit ratings behemoth. A peer to Bloomberg but a very different beast where product and service overlaps are limited.

‘MIKE’ DROP

There are two questions which the financial industry must be asking:

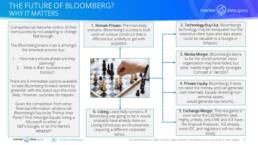

1.What will be the future business structure? As outlined in the MDG graphic a private structure is the most likely outcome.

2.Then the next question comes into play, where is Bloomberg’s business heading?

Each is naturally intertwined with the other. What has gone unremarked is the progress of internal change in middle management. The original guard is fading away and in the last two years there has been an influx of new blood in these middle ranks tasked with transitioning the company to the future. I would argue this is more profound than changes at the top. As Bloomberg has grown the original micro-management has had to give way and as these middle managers rise their impacts will become more pronounced. However there are challenges.

The name of the terminal ‘Bloomberg Professional’ describes exactly Bloomberg’s client base, other than wealthy individuals, only institutions can afford their services. Despite Bloomberg’s ability to add new terminal subscriptions this is a finite market, and its two other main product areas are highly competitive, i.e. ‘B-Pipe’ datafeeds and ‘Bloomberg Data Licence’ where the alternatives cannot be described as inferior. Adding new data sources has become an incremental process by time and revenues, the main ones already long onboard, though primary commodity and energy markets are still virgin territory but dominated by players who prize and protect their data and trading services.

Other markets which are opening up include retail and mass media, however these markets are low margin, reluctant spenders at best.

Which brings the business back to where Bloomberg gained its initial competitive advantage, being the first Cloud. The demand for the ability to process data and analytics in a cheaper third party environment is growing, and a core reason Big Tech is partnering the likes LSEG/Refinitiv and S&P Global. As the operational and IT costs of business rise, banks already have an alternative in place, Bloomberg.

This is why the future of Bloomberg matters, by outsourcing critical elements of their investment infrastructure financial institutions big and small have become dependent upon Bloomberg to function operationally.

Keiren Harris 03 May 2023

For information on our consulting services please email knharris@marketdata.guru

www.marketdata.guru/data-compliance

Please contact info@marketdata.guru for a pdf copy of the article

#marketdata #bloomberg