2.3 Information Providers: Leadership from East Coast to West Coast

Just as organisms have evolved from humble single cell beginnings to the complex structures of today, market data as an industry is evolving. Just like life there are periods of steady evolution, there are also periods of sudden revolution.

Whereas up until now there has been evolution, now we are seeing revolution.

An interesting question is, are the big beasts of the market data industry such as Bloomberg and Thomson Reuters dinosaurs heading towards extinction with the oncoming Cloud Technology asteroid or other unseen catastrophe?

For now, their demise appears unlikely. While shackled to legacy technologies and managements that find it hard to be reactive, let alone proactive, dynamically, they have the consolation their biggest clients are in the same position.

What is clear is that the large market data vendors have evolved in linear environments, through organic growth like Bloomberg whose prime business is terminals, or mergers like Thomson Reuters and Interactive Data, itself now subsumed into ICE Data. They now have to adapt to a more multi-dimensional universe.letera

Average revenues for the leading information providers business year ending 2015:

- The Top 6 Billionaire’s Club US$4,965 Million

- The Tier 2 (Next 5) Club US$506 Million

- Average for combined 11 US$2,938 Million

Of the top 6 vendors leading vendors today, all are headquartered in the United States, with the exception of IHS Markit with its operations run out of London, but it is listed on NASDAQ with major shareholders being American.

The ownership and location of the leading information providers is a reflection not only of where power is concentrated in the market data industry itself but a correlation of the development of global financial markets and media, i.e. where the money is, or at least was.

Of the US companies, all except Factset (Norwalk) and Morningstar are based in New York. Interactive Data headquarters are in Bedford, Massachusetts, but the decisions are made in New York.

Inevitably the market data industry has revolved around New York and London, and other markets seen through the prism of this axis. It is dominated by English language products and services catering to the preeminent 2 global financial centres.

But what about going forward? Amazon and Microsoft are based in Seattle, while Google is in Silicon Valley, not that far from Stephane Dubois’ market data upstart, Xignite.

These are West Coast companies, with different world views, and their financial information business’ which now and in the foreseeable future are components of larger business universes. However, their financial markets sales offices are based in New York.

Is FinTech Industry Development an Indicator?

While FinTech covers a multitude of offerings, very often unrelated to market data directly, and aimed as much at the retail as institutional market, it could well be an indicator of where the market data business dynamics will be shifting.

FinTech is not only a consumer of information, it is also a creator in its own right as it generates output based upon analytics and statistics.

If FinTech is a leading indicator as to the future ‘balance of power’ as a consumer and source then there is merit in assessing the current state of development in the FinTech market.

Defining FinTech markets is somewhat subjective, therefore available statistics and analysis can be broad. However, there has been good research.

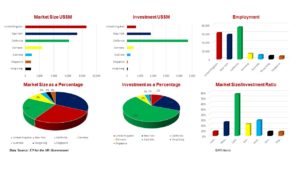

In 2016 EY produced a report of the top 7 FinTech global centres for the UK Government. In summary, these accounted for:

- Market Size US$26,780 Million.

- Investment US8,060 Million

- Employment 230,000

Source EY, Figures in GB£ 2016 with US$ X-Rate 22 May 2017

When market size and investment figures are looked at more closely it shows existing FinTech centre leaders UK, and New York are seriously lagging California in investment.

Key Points:

- While the UK is the single biggest market, it has low investment to market size rate.

- The US is the largest single country market, with a far higher ratio of investment to existing market data size.

- Employment is highest in California and combined with investment indicates a substantial growth in potential knowledge base.

- China and Japan were not included in the study.

Is this a portent of things to come in the world of financial information and market data? After all, many FinTech innovations are data driven.

Crystal Ball

- Linear concepts of market data services, management, and relationships will continue to be a feature, but going forwards as only as a strand within a multi-faceted relationship system.

- The existing leading market data vendors’ dominance is not under threat from within the industry, their future challenge is coming from without.

- Outside challenges come at both the top end and the bottom end of the market.

- At the top end, the challenge will be led by content seekers such as Amazon and Google based on new technologies reaching new audiences and breaking down cost barriers that currently exist within the market data industry as it now stands.

- At the bottom end the new players are the FinTech companies whose perception of the market place is going to be broader than just institutions, but encompass the retail market ranging from High Net Worth Individuals to the Mass Affluent.

- These are outsiders moving in, and to an extent this has happened with IHS merging with Markit, and The ICE’s purchase of IDC, S&P’s evaluated bond pricing service, and Super Derivatives.

- The future leaders within the industry will still be overwhelmingly American, though more likely to be based on the West rather than the East coast.

Importantly these new players coming to the financial information industry have fundamentally different mindsets to a Bloomberg, or a Thomson Reuters. Their world views are shaped by different environments in concept and application.

They are not likely to be limited by the boundaries of the financial institutions, but see their consumer base from the individual retail investor up. This is as true for a Google or a start-up.

This raises the questions, where does the development of the financial information industry lie? Is it with the Moreton Steakhouse (i.e. a Bloomberg) or MacDonald’s Hamburgers? Perhaps they will co-exist?