4.3 Business Strategies for Data Sources (Exchanges)

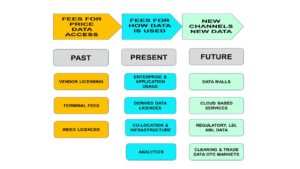

Stock Exchange’s business strategy has progressed in 2 clear stages up till now, firstly through charging fees for access to data, then by developing fees for how that data is being used. These trends will continue, as exchanges will strengthen their contracts and therefore revenue as they search to increase income from both access and usage.

The first two stages in building a market data business strategy have generally held true for most exchanges, although some like Deutsche Bourse, London Stock Exchange, and NASDAQ OMX have also become vendors, in their own right, with varying degrees of success.

Evolution

What has and is happening is movement up the value chain from the provision of basic price data, partly driven by market saturation, to the second generation of value added data such as analytics, and enterprise usage.

The leading exchanges are now focusing on the third generation based upon a new client base accessing data in new ways, and importantly the growth of regulatory mandated market data, for which exchanges are ideally placed to take advantage of.

This is likely to be marked by less overall reliance by the exchanges upon market data vendor, as the symbiotic relationship which has existed between the two partners is becoming less close and adapts to what is happening in the market place.

New relationships are already being forged, for instance London Stock Exchange in 2012 agreeing to provide prices to Google, and the LSEG’s messaging layer tie up with Solace.

A Failing Strategy?

Data needs a home, and data centres are designed to provide it. These are vital cogs in the modern connectivity chain.

In the last 10 years, exchanges have invested heavily in data centres to provide paid for infrastructure services, co-location for high frequency trading, and offer other services. For instance, in 2013 HKEx invested US$200 Million in a new centre, following on from large developments by NYSE and others.

While it is easy to understand the practical logic of exchanges entering the infrastructure facilities space, it is increasingly hard to apply an equivalent business logic. These facilities are expensive to build, expensive to maintain, expensive to keep up to date, and arguably not even core to an exchanges’ main business, and it is widely rumoured none have yet to meet expectations.

The infrastructure facilities business is definitely profitable, and dominated by successful players such as Switch, Savvis, and Equinix, the last of which themselves in 2016 admitted are under pressure from smaller competitors, resulting in a one day share drop of 4%.

In addition, the advent of the Cloud has brought a raft of highly capitalised companies into the market space with more money, larger client base, and better technology than any exchange can bring to bear.

Like Banks who think they are really IT companies, perhaps Exchanges should focus on what they do really well, and leave infrastructure to the specialists, or at the very least develop partnerships. The data centre strategies of exchanges could prove a costly long-term distraction.

Snap Shots in Time: Contracts & Licences

The exchange’s ability to maintain control over their prices will continue to underpin basic revenue flows and protect profitability, but their overall market data businesses need to adapt.

For instance, contracts governing market data usage as part of licences only reflect a snap shot in time, i.e. the date they were written. As these contracts are rarely updated they quickly cease to reflect market realities, as the consumers always find new ways of utilising market data which are not covered by these agreements.

To be fair, predicting future usage in today’s environment really does need someone who can accurately predict the future.

Future Strategies

Future strategies will have to be more fluid as the exchanges seek to create higher margins through opening up new and innovative channels to reach their clients directly, in addition to, but not supplant traditional market data vendors, for instance using Cloud based solutions.

Equally regulation will in the aid development of new market data products, firstly through providing information around the legal and compliance status of companies listed on their boards. Secondly by regulators further driving the reporting of OTC market trades to established reporting venues, i.e. exchanges.

Many exchanges have yet to realise their unlocked potential in the pricing data they hold.