4.2 How Exchanges Make Money from Market Data

The core of the information services of exchanges is the provision of traded and tradable data direct from their own venues.

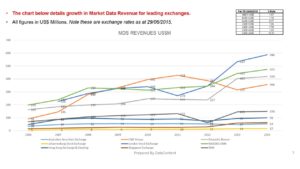

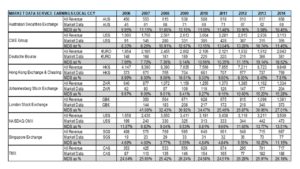

- In 2007 market data revenues for 9 leading exchanges totalled US$1,144 Billion.

- By 2014 this had increased to US$2,203 Million, i.e. 93%.

- By 2015 the exchange with the largest information services revenue is the London Stock Exchange with revenues of US$586 Million (£373 Million) on overall turnover of US$2,170 Million (£1,381 Million), representing 27% of the total business.

- As a percentage of overall revenue, information services is growing more important to exchanges.

- The percentage of turnover, other than the LSE varied from a low of 8% for Hong Kong Exchange & Clearing to 26.2% for TMX Group which is known for its aggressive compliance audit.

- In comparison Year Ending 2006 saw a range in percentage of turnover from 7% for the Singapore Exchange to 24.6% for TMX.

- For the 8 exchanges, other than LSE the percentage of revenue generated grew from an average of 8% in 2006 to 12.7% in 2015.

Importantly the growth not only came from data sales, it also comes from the provision of value added services such as analytics, and technical infrastructure services such as co-location.

Indices are also a major revenue generator either through licensing, or their own in-house index creators, notably LSE’s FTSE Russell and Deutsche Bourse’s STOXX.

An additional factor is that unlike commission and IPO fees, information services provides a far more stable revenue stream. This means many exchanges’ management place an increasing emphasis on generating revenue from information services and associated technology services.

What is often forgotten is that the infrastructure required to create the market data business for exchanges are mostly sunk costs. The exchanges must provide the information services to the market and have in place the technology to do so, therefore by

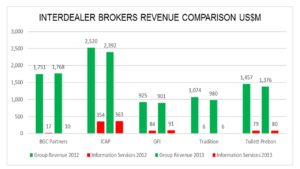

Inter-Dealer Brokers

In contrast to the exchanges, for Inter-Dealer Brokers, in 2013 had estimated revenues for all activities of US$7.4 Billion, and broker data revenues including post trade, risk, and analytics contributed US$550 Million, i.e. 7%. The key difference with exchanges is that the IDBs were until the TP/ICAP merger and BGC takeover of GFI competing strongly in OTC markets data.

There is now a lot less competition as the two large remaining entities strengths are not necessarily going head to head while Tradition is insignificant in the market outside Energy and Meitan in Japan.

- ICAP’s information services generated US$363 Million in all areas, including US$120 Million purely for data and Tullett Prebon Information, US$80 Million were the clear leaders in the provision of broker data.

- This lead is built upon a strong foundation of ‘all you can eat’ multi-year contracts with Bloomberg and Thomson Reuters.

- Core revenue streams flow from market data vendors who re-distribute to their own clients.

- A key growth area is enterprise style agreements which allow financial institutions to use data firm wide, especially for application usage.

- Value added services like analytics, risk, and trade data, and providing stronger revenue streams.

- Once broker data has been established in applications such as risk management it becomes very hard to displace owing to the effort required. Therefore, becomes a stable revenue stream.

- Broker data sales reinforces the brokerage business, as clients like to source data from the brokers they deal with.

- BGC sold its eSpeed business to NASDAQ in 2013 resulting in the revenue drop. Since then BGC has focused on new deals with vendors and enterprise licences with financial institutions.

- Sources 2013 Accounts. Tradition is an estimate as TFS did not separate data revenues out during this period.

The figures provided here are from 4 years ago, there has been a number of merger and acquisition changes, which impacts trend analysis.

Despite the undoubted success of the leading IDB’s information business, smaller brokers, especially in the Commodities and Energy markets have yet to embrace opportunities to monetise their price and data assets.

Summary

Market Data is a high margin, profitable business for sources such as Exchanges and IDBs, however with market saturation at the basic price level the challenges lie in growing that business into new areas such as analytics, regulatory information, and leveraging so far under-utilised internal price data.