4.4 Dollar Value of Proprietary & Unique Data

There is a certain inevitability that as in other fields of business, certain types if market data command a greater return than others. Often the value placed is a function of its uniqueness or accessibility, even brand.

Subjectively, but based on premiums paid by financial institutions, I have divided services into 3 base groups. Others will naturally have different and equally valid opinions.

Naturally within a specific segment there are going to be higher and lower value services. For instance, MSCI commands a significant premium over say NASDAQ Indices. As one Funds Service Manager, half-joked to me ‘negotiating with MSCI over subscriptions is just a matter of working out how large the price increase will be’.

Also, different types of asset class data have greater value than others, but that has not been reviewed here, but as an example FX data can now be sourced cheaply and comprehensively from a wide range of suppliers, however, access to high quality US Treasury data comes at a significant price.

Equally different businesses will place different values on different data sets, for instance a Treasury House will regard Foreign Exchange data as a must have, whereas for an equity house, it may be important, for instance when pricing overseas, or if FX rates have an economic impact, but then news of rate changes could well have a greater value.

What the business does drives the relative value of specific types of information and market data to that business, and this varies significantly depending on market participation, and available choice.

What is required is more than superficial knowledge of the business by both vendors and internal procurement to avoid delivering sub-optimal solutions to the end users of market data.

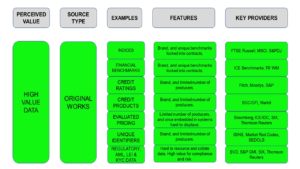

High Value Data Features:

- Original works provides high value added unique market data.

- The business decision to subscribe is not discretionary, but the information is considered to be a ‘must have’ without which the business either cannot function, or cannot compete.

- The specific data is difficult to replace owing to links to commercial contracts, for instance, how a fund manager benchmarks to a specific index for performance.

- Often the provider is perceived as ‘arrogant’ and difficult to deal with, and unsurprisingly, too expensive. Markit and MSCI seem to generate the most comments in my experience.

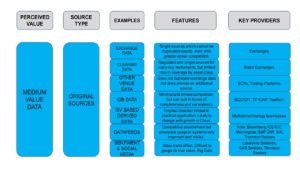

Medium Value Data Features:

- There are a limited number or even single sources of original data.

- However, there are multiple channels from source to end user. This is where market data vendors play a crucial role in cost control through their competition.

- While sources like exchanges rarely compete directly with each other they must not raise prices too high and deter financial institutions from subscribing.

- This is particularly true of exchanges reliant upon a high direct retail investor base, as those mass affluent punters are highly price sensitive. So many exchanges adopt a strategy of discriminating between professional investors and retail investors. An example is NASDAQ’s US$1 per month for a non-professional subscription to OpenView and US$6 per month for a professional subscriber.

- A relatively new but interesting source for data is social and sentiment, for example Thomson Reuters development of an analytics service to track Twitter updates.

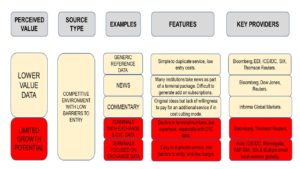

Lower Value Data Features:

- Source data usually comes without an associated and costly data licence, for instance historical price data (Though importantly not tick histories).

- Other data such as capital changes, corporate actions, director’s dealings are public knowledge, therefore there may not be any sourcing fees.

- Services such as reference data can be operated and managed from centres with low labour costs, i.e. India, as there is a surprising level of manual work required.

- It means there are lower barriers to entry in terms of cost, and the market is highly competitive at the bottom end.

Why might News be considered low value when so important to the markets?

- All a question of cost, Bloomberg, Thomson Reuters, (plus Nikkei/Quick in Japan) bundle the news service into their terminal offering which between the big 2 accounts for around 60% of the market.

- Combined with Bloomberg and Thomson Reuters global coverage and (for the most part-they have their off days) undoubted quality, it is hard to justify adding say an individual Dow Jones Newswire on top at say US$100 PM, even if DJN offers a better service.

- This creates a high hurdle for other newswires to enter the market.

- In addition, it puts other terminal providers without their own in-house news wire at an immediate, significant content and cost disadvantage.

Limited Growth Potential:

- As already discussed the decline in terminal numbers institutionally is having a detrimental effect on Bloomberg and Thomson Reuters.

- The exchanges will also lose out to an extent in that these are professional users paying the highest terminal fees, but this revenue stream is being supplemented and exceeded by other forms of revenue flow, such as non-display, derived data, and original works licences.

Return on Data Investment (RODI)

RODI is a term first coined by Rafah Hanna to measure the investment value of the market data services to the consumer.

Theoretically, consumers and vendors should have a functional policy of constantly validating their market data sources throughout the contract life cycle to measure the true business benefits of market data as a resource which provides direct benefit to the bottom line. The motivations ought to be:

- Best practice data governance.

- Cost control.

- Quality assurance.

- Assessment of future requirements and alternatives.

In reality, and for reasons which are at the same time both understandable and inexplicable, few organisations have in place truly comprehensive strategies for managing market data through the contract life cycle.