1.3 Changing of the Guard?

New technology is bringing new market entrants to the market data space, including the likes of Amazon, Google, IBM, Microsoft, and Tencent. These are the 5 ‘new’ players looked at in the tables below. Equally there are companies such as Accenture and Alibaba which should not be ignored.

There is a commonality: they can deliver technology, services, and information content across the market data and information spectrum through their Cloud-based services. While not aggregators in the traditional sense, they are enablers which can act like an information supermarket by creating shop windows for information providers. While not, at the moment, directly competing in the aggregation space they are becoming competitors with greater reach than the traditional information providers without being tied to legacy environments. Though it has been reported Google is in the process of developing a GUI specifically for displaying market data.

Exchanges, content providers, analytics and newswires are all taking advantage of this reach to make their services available to a broader range of customers than was previously available to them.

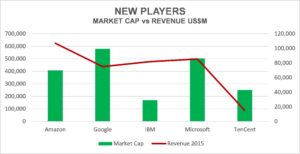

In pure financial terms, there is a major disparity between the financial numbers of these new potential players and the traditional vendors.

- The 12 leading Information Providers total revenue year ending 2015 was US$44.6 billion with an estimated market capitalisation of US$215.1 billion (as at 3 March 2017).

- In comparison, the 5 potential new players had total revenue year ending 2015 of US$364.0 billion with a market capitalisation of US$1,909.8 billion (as at 3 March 2017).

- The 5 new players have vastly more potential financial firepower with 2x more revenue, and 8.9x greater market capitalisation.

Source: Thomson Reuters & DataContent

What is happening to the Information Providers?

- The traditional vendor is in decline. Bloomberg’s revenues are not growing as they once were, and Thomson Reuters combines the apparent lack of a long-term strategy with years of relatively static income. Other players are growing faster, with good reasons why.

- Smaller vendors have been swallowed up by new entrants to the direct market data business but which have synergies including looking to leverage proprietary data, i.e. ICE acquired Interactive Data, and his acquired Markit. Who is next to be assimilated?

- Increased value of proprietary data, i.e. Markit Red Codes, Indices, specialist data. This data while it has always carried a premium, has become even stronger thanks to specific benchmarking. Though in future regulators may seek to control abuse.

- Contractual obligations and Intellectual Property Rights (IPRs) are a licence to print money, and those that know it like Exchanges, Index Creators, and others fiercely police and protect their assets.

- Expect growth in auditing and compliance, across the globe outside the Top Tier Banks, especially for ISV’s, original works creators, and retail institutions.

- Ever more and more intrusive regulations drive market data requirements, though for some reason there is a disconnect in that many users do not correlate the two. FRTB being a good example.

- Big dealing rooms are out, electronic trading is in, requiring fewer seats, combined with the big banks cutting costs.

- Reduced terminal numbers are a consequence, and they look to be in ‘terminal’ decline within the institutions.

- Margins being low it switches emphasis to use of market data in pre-trade and post-trade applications, analytics and decision making tools.

Will new players enter the market data industry and what are the benefits to them?