3.1 THE MARKET DATA YELLOW BRICK ROAD

Connectivity, Content, and Market Access, i.e. trade. These basic concepts are all are in the process of undergoing significant transformation that directly affects how financial institutions make their money, and in turn how the financial information vendors need to adapt to service their clients.

There is a simple rule ‘No Market Data, no financial markets participation’. Data on market levels is fundamental to making the decision of “Shall I buy? Shall I sell?”

It has been argued that L. Frank Baum’s “Wizard of Oz” was an allegory for economic change in the 1890’s United States, with the Yellow Brick Road representing the Gold Standard and Silver Slippers the Silver ratio. The Market Data Yellow Brick Road is all about access to information, and importantly act upon the information available.

Fortunately, there is always a way to connect to the market, from a Bank’s sophisticated electronic trading platform to a retail investors’ humble phone, but when and when and where there is a lack of price discovery it usually leads to a money losing game of ‘Blind Man’s Bluff’.

Anecdotally, I did have one proprietary trading client whose systems failures kept it out of the market for a period and during that time their performance improved.

Financial Institutions Changing Needs

Crucially, what is different now, and the trend is accelerating, is the new and diverse ways information can firstly be fed into the business and secondly, how it is distributed around the business, and for what purpose. It is these changing dynamics which are forcing changes in the institutional and the retail markets.

As we shall see market mechanics and profitability are the natural driving forces of change. There are no hard concepts to identify, just plain common sense trends.

- The more liquid a market, the more competitive it tends to be which drives down commission margins. It also makes price discovery easier, in turn driving down the cost of market data.

- The infrastructure effect of a more liquid market is that it becomes easier to create electronic platforms for trading.

- Because electronic Direct Market Access (DMA) is cheaper, and more efficient, than brokers on the desk, the knock on leads directly to increased competitiveness, along with the displacement of brokers on the desk with their own terminals by feeds.

- This leads to the entire trading cycle becoming electronic utilising systems populated by market data fed by feeds.

There is also one outside driver in tomorrow’s market data world, and that are the regulators whose rules increasingly foster the growth of reference data services, and electronic trading. Regulators are naturally driven by the requirements of their home markets and the relative sophistication of those markets, therefore the global trend is to mimic the main features of the US, European and UK markets.

MiFID2, the Fundamental Review of the Trading Book, the IOSCO Principles on Financial Markets are all having wide ranging consequences regarding the sourcing of market data, how market data is and can be consumed, and in turn providing pricing, and price discovery, to the market.

In information terms and market data requirements, this means the following:

- Preference for tradable pricing, with greater emphasis on prices generated via electronic platforms.

- Wider use of voice recognition software to capture over the phone prices, which is becoming increasingly useful in covering illiquid markets.

- Due diligence in sourcing prices for reporting use.

- Ensuring audit trails and price histories are accessible and complete.

- A subtle but important switch from ‘How to Source’ requirements, to a more interventionist ‘What to Source’

- A greater emphasis in the value of proprietary and unique data only available from a single source or limited number of sources.

The leading market data vendors are well aware of these changes, and have set up highly skilled teams to develop products and services to meet their clients demanding needs.

However there seem to be issues:

- The market data vendors tend to focus on the large Tier 1 financial institutions at the expense of smaller institutions.

- Banks themselves tend to be slow in identifying the market data issues relating to natural changes in the markets, plus those which are happening by regulatory fiat.

- Increasingly Banks investment in market data resources seem to be driven by risk, compliance, and reporting requirements.

- This is changing the nature of who makes the decisions to source market data within a Bank and the reasons for making those decisions.

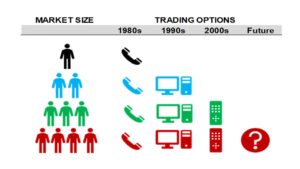

The Revolution in the Retail Space

There is a tendency to forget the increasing numbers of high net worth individuals and the newly mass affluent which now trade thanks to the Internet. It tends to be hidden because their market data consumption as is usually indirect, i.e. vendors supply online brokerages with a feed, who then provide a retail broking service, or provision of market data to online portals. The intermediaries taking a business decision to absorb these costs.

Unsurprisingly retail clients are very price sensitive, and they do not trade as much, nor in large sizes, and when they do must go through a broker. To cater for this many exchanges provide a different cost structure for retail ‘non-professional’ users, such as NASDAQ which charges a US$1 per month fee for such users.

These retail users do not require the depth of market data required by their professional counterparts so are willing to settle for the basic Bid/Asks (Level 1) rather than pay for the complete order books (Level 2 and above).

The retail market is expanding, and these clients are becoming more sophisticated. Where the non-professional investor once looked no further than trading plain vanilla domestic equities, they are now more adventurous. Result is their brokers offer a broader range of investment opportunities.

However, the provision of market data services are cheap and margins are low with fairly lower barriers to entry. But importantly there is a shift in quantity and quality occurring in providing market data to this space. Smaller market data vendors catering for the retail market have never succeeded in gaining the critical mass necessary to build strong businesses but

This looks like developing into the question of different viable business models to cater for the institutional market and/or the retail market.

In Summary

The question becomes what paths should market data vendors and information providers take when there are no obvious road maps?